Facts:

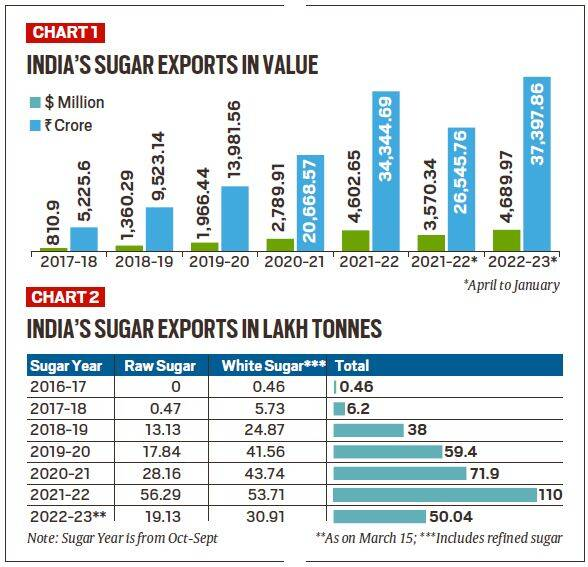

- Between 2017-18 and 2021-22, sugar exports have soared from $810.9 million to $4.6 billion, and could cross $5.5 billion - or Rs 45,000 crore - in the fiscal year 2022-23.

- The increase is even more significant in quantity terms. During the 2016-17 and 2017-18 sugar years (Oct-Sept), India’s shipments were a mere 0.46 lakh tonnes (lt) and 6.2 lt respectively, which zoomed to 110 lt by 2021-22.

- Chart below shows the value of sugar exports from India in US Dollars and Rupees (2017-18 to 2022-23), increasing year-on-year except in the 2021-22 period.

- India’s exports of both raw and white sugar. Chart below shows the quantity in lakh tonnes from 2016-17 to 2022-23. Till 2017-18, India hardly exported any raw sugar.

- The efforts to push exports of raws got a further boost when Indonesia, in December 2019, agreed to tweak its ICUMSA norms to enable imports from India.

- The Southeast Asian nation previously imported only raw sugar of 1,200 ICUMSA or more, largely from Thailand. Those levels were brought down to 600-1,200 to allow its refiners to process higher purity raws from India.

- Out of India’s total 110 lt sugar exports in 2021-22, raws alone accounted for 56.29 lt. The biggest importers of Indian raw sugar were Indonesia (16.73 lt), Bangladesh (12.10 lt), Saudi Arabia (6.83 lt), Iraq (4.78 lt) and Malaysia (4.15 lt).

- The country also exported 53.71 lt of white/ refined sugar, the leading destinations for which included Afghanistan (7.54 lt), Somalia (5.17 lt), Djibouti (4.90 lt), Sri Lanka (4.27 lt), China (2.58 lt), and Sudan (1.08 lt).

What are Raw and White Sugar:

- ICUMSA (short for the International Commission for Uniform Methods of Sugar Analysis), is a measure of the purity of sugar based on colour. The lower the value, the more the whiteness.

- Raw sugar is what mills produce after the first crystallisation of juice obtained from crushing of cane. This sugar is rough and brownish in colour, with an ICUMSA value of 600-1,200 or higher.

- Raw sugar is processed in refineries for removal of impurities and decolourisation. The end product is refined white cane sugar having a standard ICUMSA value of 45. The sugar used by industries such as pharmaceuticals has ICUMSA of less than 20.

- Till 2017-18, India mainly shipped plantation white sugar with 100-150 ICUMSA value. This was referred to as low-quality whites (LQW) in international markets.

Why are Raw Sugar Exports preferable?

- Ease of Transport and Distribution: Much of the world sugar trade is in ‘raws’ that are transported vessels of 40,000-70,000 tonnes capacity as it requires no bagging or containerisation and can be loaded in bulk. The buyer of raw sugar is the refiner. Whereas, ‘Whites’ are usually packed in 50-kg polypropylene bags and shipped in 12,500-27,000-tonne container cargoes over shorter distances. The buyer of white sugar is the end-consumer.

- Time Window: The refineries in countries such as Indonesia, Malaysia, South Korea, China and Bangladesh imported raws from Brazil. Brazilian mills operate from April to November, whereas our crushing is from October to April. We told them that they could source our raws during Brazil’s off-season.

- Freight Cost Savings: The voyage time from Kandla, Mundra or JNPT to Ciwandan Port of Indonesia is 13-15 days, compared to 43-45 days from Brazil’s Port of Santos.

- Specific advantages of Indian raw sugar:

- Dextran free raw sugar: Dextran is a bacterial compound formed when sugarcane stays in the sun for too long after harvesting. Indian raw is produced from fresh cane crushed within 12-24 hours of harvesting. The cut-to-crush time is 48 hours or more in Brazil.

- Supply of raw sugar with a very high polarisation of 98.5-99.5%: Polarisation is the percentage of sucrose present in a raw sugar mass. The more the polarisation — it is only 96-98.5% in raws from Brazil, Thailand and Australia — the easier and cheaper it is to refine.

- Enhanced awareness about the quality of Indian raw sugar: enables our raws today fetch a 4% premium over the global benchmark (New York No. 11 futures contract) price. This is in contrast to white sugar as our LQW sells at a $40/tonne discount to the world price (London No. 5 futures).

Challenges:

- Dwindling availability for domestic market: Year-end stocks of sugar with Indian mills peaked at 143 lt in 2018-19. The concerted export drive, coupled with diversion of sugarcane juice to produce ethanol for blending with petrol, helped bring down closing stocks to about 70 lt by 2021-22 which was enough for just over 3 months of domestic consumption. This is in contrast to 2017-18, where closing stocks of sugar at 105 lt enabled stocks accumulation to 5 months of domestic consumption.

- Caps on Exports: Lower stocks and production dipping to an estimated 334 lt (from 359.25 lt in 2021-22) has led the government to cap India’s exports in the current sugar year to 61 lt. Out of that, over 50 lt have already been dispatched.

- Reduced price realisation of sugar farmers: Mills in Maharashtra are now realising around Rs 32 for every kg of sugar sold in the domestic market. As against this, London white sugar prices are ruling at $585 per tonne. Even after factoring in the $40/tonne LQW discount and deducting Rs 2,500-3,000/tonne of internal transport and port expenses, the ex-mill realisations from exports work out much higher, at Rs 42-42.5/kg.

Way Forward:

- The government may be concerned about domestic availability and food inflation. But overseas markets lost aren’t easy to regain.

- Building export markets takes effort. Overseas buyers need to be convinced about the price competitiveness, product quality, and reliability of supplies from the exporting country.