Production Linked Incentive refers to a rebate given to producers. This rebate is calculated as a certain percentage of sales of the producer (sales referred in it can be total sales or incremental sales).

For example, the PLI scheme for the Electronics Sector offered a rebate of 4-6% on the incremental sales of the producer.

The incentives, calculated on the basis of incremental sales, range from as low as 1 per cent for the electronics and technology products to as high as 20 per cent for the manufacturing of critical key starting drugs and certain drug intermediaries.

Key features of the PLI Scheme

The scheme is outcome-based, which means that incentives will be disbursed only after production has taken place.

The calculation of incentives is based on incremental production at a high rate of growth. In some sectors such as advanced chemistry cell batteries, textile products and the drone industry, the incentive to be given will be calculated on the basis of sales, performance and local value addition done over the period of five years.

The scheme focuses on size and scale by selecting those players who can deliver on volumes.

The selection of sectors covering cutting-edge technology, sectors for integration with global value chains, job-creating sectors and sectors closely linked to the rural economy, is highly calibrated.

Also, the design of the earlier PLI scheme for electronics is such that it is compatible with World Trade Organization commitments as the quantum of support is not directly linked to exports or value-addition.

Sectors Covered under PLI Scheme (14 Sectors)

Key Starting Materials (KSMs)/Drug Intermediates (DIs) and Active Pharmaceutical Ingredients (APIs): Department of Pharmaceuticals

Manufacturing of Medical Devices: Department of Pharmaceuticals

Pharmaceuticals drugs: Department of Pharmaceuticals

Large Scale Electronics Manufacturing: Ministry of Electronics and Information Technology

Electronic/Technology Products: Ministry of Electronics and Information Technology

Telecom & Networking Products: Department of Telecommunications

Food Products: Ministry of Food Processing Industries

White Goods (ACs & LED): Department for Promotion of Industry and Internal Trade

High-Efficiency Solar PV Modules: Ministry of New and Renewable Energy

Automobiles & Auto Components: Department of Heavy Industry

Advance Chemistry Cell (ACC) Battery: Department of Heavy Industry

Textile Products: MMF segment and technical textiles: Ministry of Textiles

Specialty Steel: Ministry of Steel

Drones and Drone Components: Ministry of Civil Aviation

PLI Scheme for IT Hardware

The PLI for IT hardware such as laptops, tablets, all-in-one computers, and servers was first announced in February 2021 with an initial outlay of around Rs 7,300 crore over a period of four years.

Under the scheme, domestic players investing Rs 20 crore and clocking sales of Rs 50 crore in the first year, Rs 100 crore in the second, Rs 200 crore in the third, and Rs 300 crore in the final year, would pocket incentives of 1-4 per cent on incremental sales over 2019-20, the base financial year.

The first version of the scheme was a laggard with only two companies – Dell and Bhagwati – managing to meet first year’s (FY22) targets, and the industry called for a renewed scheme with an increased budgetary outlay.

Revised Scheme

The Union Cabinet cleared a revised production linked incentive (PLI) scheme for IT hardware with an outlay of Rs 17,000 crore, which is more than double the budget of the scheme that was first cleared in 2021.

Implementation: The scheme will be implemented from July 1, with a cap on maximum incentives available to participating companies.

Tenure: The tenure of the new scheme has been fixed for six years and the Centre is expecting an investment of over Rs 2,430 crore as part of it.

Expected Outcome: The expected incremental production value could touch Rs 3.35 lakh crore, and the scheme could generate 75,000 direct jobs – in total, the employment figure could touch 2 lakh when accounted for indirect jobs.

Coverage: Investments made by eligible companies in contract manufacturers and for attaining exclusive arrangements with component manufacturers will also be considered under the scheme.

Investment: It is worth noting that under the previous PLI scheme, the expected investment was pegged at Rs 2,500 crore – under the renewed plan, that projection has been reduced (to Rs 2,430 crore) despite sweetening the incentive structure.

Incentives: The average incentive over six years will be about 5 per cent compared with the 2 per cent over four years offered earlier. Companies that locally manufacture certain components including memory modules, solid state drives and display panels will also get additional incentives under the restructured scheme. There will be flexibility in choosing the base year as well.

Cap: While the final policy with its specifics is yet to be released, it is understood that for global companies, the maximum incentive has been capped at Rs 4,500 crore, Rs 2,250 crore for hybrid – which have an element of both global and domestic entities – and Rs 500 crore for domestic companies.

Analysis of the Scheme

The PLI scheme was conceived to scale up domestic manufacturing capability, accompanied by higher import substitution and employment generation. The government has set aside Rs 1.97 lakh crore under the PLI schemes for various sectors and an additional allocation of Rs 19,500 crore was made towards PLI for solar PV modules in Budget 2022-23.

As of December 2022, 650 applications have been approved under 13 Schemes and more than 100 MSMEs are among the PLI beneficiaries in sectors such as Bulk Drugs, Medical Devices, Telecom, White Goods and Food Processing.

The electronics industry continues to ascend in importance as its applications become pervasive, particularly in the socio-economic development of a country. Electronics, supported by continuously improving communication services, will significantly enhance productivity, efficient service delivery, and social transformation.

The domestic electronics industry, as of FY20, is valued at US$118 billion. India aims to reach US$300 billion worth of electronics manufacturing and US$ 120 billion in exports by FY263, supported by the vision of a US$ 1 trillion digital economy by 2025. Improvement in manufacturing and export over the past five years ensures that India is on the right trajectory to achieve this target.

Electronic goods were among the top five commodity groups exhibiting positive export growth in November 2022, with the exports in this segment growing YoY by 55.1%.

The major drivers of growth in this industry are mobile phones, consumer electronics, and industrial electronics. In the mobile phone segment, India has become the second-largest mobile phone manufacturer globally, with the production of handsets going up from six crore units in FY15 to 31 crore units in FY22. These numbers are expected to improve as more domestic and global players set up and expand their bases in India.

Participation in the PLI scheme will help many more domestic players to attain economies of scale in production through localising. Hence, this will further enhance export competitiveness and increase India’s participation in the global value chain.

As one of the earliest ones, the ministry of electronics and information technology’s PLI scheme for large-scale electronics manufacturing (LSEM) saw successful results, with 97% of mobile phones sold in India now being made in India. Furthermore, they are also being “Made in India for the World” as we witness a sharp growth in smartphone exports by 139% over the last three years.

As of September 2022, the PLI scheme for LSEM attracted investments of ₹4,784 crore, with a total production of ₹2,03,952 crore, while also generating 41,000 additional jobs. In the medium-term, the scheme is expected to bring in additional production to the tune of ₹10.69 lakh crore and generate 700,000 jobs.

Similar successes are replicated in the pharma sector PLI with 35 imported active pharmaceutical ingredients or key chemical inputs for drugs being developed in India. In addition, other sectors, such as food products, telecom and networking products, and drones are reporting successes with visible growth in investment, employment, and production. Over 600 foreign and domestic firms have been selected across 14 key sectors in two years, indicating enthusiastic industry participation.

Benefits of PLI Scheme

The renewed scheme could attract big global IT hardware manufacturers to shift their production base to India and give a boost to local production of laptops, servers and personal computers.

It focusses on expanding India’s production and presence in Global value chains of IT hardware, servers and laptops. By deepening & broadening the electronics ecosystem in India, this scheme will play a key role in catalysing India’s tech trade and in achieving the $1 trillion digital economy goal – including $300 billion of electronics manufacturing by 2025-26.

The IT hardware industry is targeted to reach a production of $24 billion by 2025-26, with exports anticipated to be in the range of $12-17 billion during the same period. This revised PLI is expected to serve as a major catalyst for both global and domestic companies aiming to establish or expand their IT hardware manufacturing operations in India.

The successes signal that the scheme is leading to the development of a potent ecosystem that is self-sustaining and thriving.

Focuses on advanced technologies: it is likely to upgrade the skills of the existing labour force.

Replace technologically obsolete machinery and make the manufacturing sector globally competitive.

Enhanced production volumes will cater to increasing consumer demand. This can be seen for telecom and networking products, where timely intervention by the scheme will enable faster adoption of 4G and 5G products across India.

With PLI in green technologies, India can pioneer green policy implementation with a reduced carbon footprint.

Better productivity will create a thrust in free trade agreements for better market access.

Increased sales will demand better logistical connectivity. The PM Gati Shakti plan provides multimodal connectivity to manufacturing zones across India, making logistics and operations efficient. Cluster parks with plug-and-play infrastructure have also been introduced to support manufacturing in different regions.

Context: The European Union’s approval this week of new deforestation regulations poses a threat to Indian exports of items like coffee, leather, paper and wooden furniture.

The regulation is part of a larger trend of “demand-side” restrictions, in which major consumers of agricultural commodities are leveraging their market share to encourage sustainable production. The United Kingdom recently approved a similar regulation, and United States lawmakers introduced a similar bill in Congress. In March, the Chinese government announced an initiative with Brazil’s largest beef lobby for deforestation-free beef exports.

What is the new deforestation regulation of the European Union?

It requires EU-based companies to ensure that their imports and exports are “deforestation-free” and uphold human rights, Human Rights Watch.

The law establishes the legal requirements for European businesses regarding biodiversity loss and human rights abuses embedded in their international supply chains.

On April 19, 2023, the European Parliament voted for the European Union Deforestation-Free Products Regulation (EUDR).

Regulations covering wood, palm oil, soy, coffee, cocoa, rubber, and cattle they import or export have not been produced on land that was deforested after December 31, 2020.

The law requires companies to trace the commodities back to the plot of land where they were produced, or, in the case of cattle, the particular locations where the animals were raised.

The regulation also requires companies to ensure that these seven agricultural commodities are produced in conditions that comply with “relevant laws” in their country of origin.

These include laws on land use rights; labour rights; human rights protected under international law; free, prior, and informed consent, as set out in the United Nations Declaration on the Rights of Indigenous Peoples; and anti-corruption laws.

Even the European companies will also have to ensure that the commodities they produce domestically comply with the regulation, raising questions about some EU member states’ practices. In Sweden, for example, the timber industry has often encroached upon land that Sami people rely on for reindeer husbandry, a practice central to their cultural identity.

Within 18 months after it enters into force, the European Commission will announce which producer countries – including EU member states – are deemed low, medium, or high risk based on their rate of deforestation and forest degradation, and the existence, compliance with, and effective enforcement of laws protecting human rights, the rights of Indigenous peoples, local communities, and other customary tenure rights holders, among other criteria.

Products from countries determined to be “high risk” will face tougher scrutiny by EU customs authorities and require European companies to conduct greater in-depth due diligence when sourcing from those locations.

Larger companies will have 18 months after the regulation enters into force to make changes to comply with the law before facing penalties for violations. The new rules will apply to large firms from December 2024 and small firms by June 2025.

Why such a move?

Deforestation is second only to fossil fuels as a global source of greenhouse gas emissions fueling the climate crisis. Globally, industrial agriculture is the most significant driver of deforestation.

Industrial agriculture has been linked to a range of human rights abuses, including forced and child labour, dangerous exposure to toxic pesticides, forced evictions and displacement, encroachment on Indigenous peoples’ traditional territories, and violence and intimidation against environmental defenders, among others.

The volume of deforestation associated with EU imports is second only to China, according to a 2021 study by the World Wildlife Fund and Trase.

For example: Nearly one-tenth (9.6 percent) of Malaysia’s sawn wood exports were headed for the EU in 2021, according to the Observatory of Economic Complexity (OEC), a trade database.

Impact on India:

Regulations would impact 479 products exported from India worth around 1.3 billion dollars.

This would make new participants in the agro-goods export-less. They would have to re-orient their policies.

Indian exporters would have to look for new markets for their products in future. This would raise the transportation costs, partnership cost and insurance cost on the exported items. Thereby hurting the exports in the long-term.

Way-forward

India along with other developing and agro-exporting countries should create a platform and negotiate with the members of the European Union.

Context: India’s goods exports for 2022-23 scaled up significantly from earlier estimates to almost $451 billion, indicating a 6.9% year-on-year growth. Similarly, the import bill as per the May 1 statement was pegged at $711.85 billion.

Experts have flagged petroleum shipments as the main driver for the high revisions of recent export data.

Source: PIB

Major exports from India:

Export trends in India show that the episodes of export growth accelerations are not new. India’s exports are characterized by a high rate of volatility making the growth path episodic with discrete shifts from periods of low growth to periods of high growth and vice versa. The switch between highs and lows is accompanied by dramatic changes in growth rates

India’s exports benefited majorly from the surge in global growth after two years of repressed demand owing to the pandemic. Several PLI schemes in diverse sectors, such as mobile manufacturing, electronic and textile products, automobile, and auto components have boosted domestic manufacturing and exports by helping India gain competitiveness in the global markets. Though these incentives take a few years to show their full effect, early signs of their positive impact are already visible.

Source: Ministry of Commerce and Industry

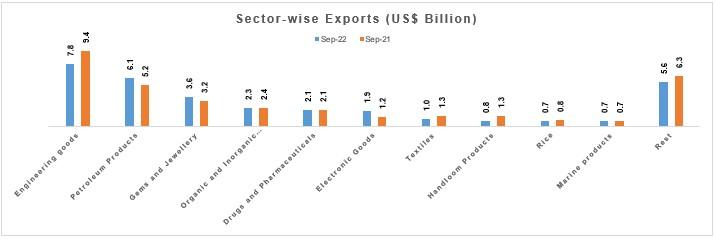

Major sector-wise exports of India include:

Engineering Goods: It registered exports at US$ 7.8 billion. This is primarily due to the benefits that the sector enjoys owing to the various trade agreements India has with other countries. Currently, all pumps, tools, carbides, air compressors, engines, and generators manufacturing MNC companies in India are trading at all-time highs with increased prospects of shifting production to India. It is expected to continue its upward trajectory in steel, auto components, and medical devices and India's push for Make in India.

Petroleum Products: Petroleum products have contributed in a major way to Indian export growth. They registered a growth of US$ 6.1 billion. Factors leading to the growth are rising crude oil prices which got aggravated by the post-pandemic world, demand spiking for oil, and the recent geopolitical tension.

Gems and Jewellery: Gems and jewellery made up US$ 3.6 billion of India's exports. This sector was one of the key focus areas of Indian exports and is expected to flourish more with the reduction of import duty on cut and polished diamonds and the Extension of the Emergency Credit Line Guarantee Scheme (ECLGS) for MSMEs, which make up 90% of the sector. The largest exports of gems and jewellery from India are to the United States of America (USA), United Arab Emirates (UAE) followed by the United Kingdom (UK), Germany, Singapore, the Netherlands, and many more.

Agriculture Exports:Agricultural exports were elated by the government’s push to meet the global demand for food amid the pandemic. India exported rice worth US$ 0.7 billion, the highest among agricultural commodities. The rise in the export of agricultural and processed food products has been largely due to the various initiatives taken by the government through the Agricultural and Processed Food Products Export Development Authority (APEDA) such as organizing B2B exhibitions in different countries, exploring new potential markets through product specific and general marketing campaigns by the active involvement of Indian Embassies.

Organic and Inorganic Chemicals:With strong demand from developed markets, organic and inorganic chemicals registered exports worth US$ 2.3 billion further contributing to the rise in Indian exports. The export growth of organic and inorganic chemicals has been achieved because of a surge in shipments of organic, and inorganic chemicals, agrochemicals, dyes, dye intermediates, and specialty chemicals. China is a major importer of dyes, dye intermediates, and organic chemicals from India. The USA remained the largest importer of essential oils, and inorganic chemicals while Brazil was the top importer of agrochemicals from India.

Electronic Goods: Electronic goods have also contributed massively to the export surge from India. The exports of electronic goods amounted to US$ 1.9 billion. The segment benefitted from several PLI schemes, such as the Scheme for Large Scale Electronics Manufacturing and the Scheme for the Promotion of Manufacturing of Electronic Components and Semiconductors (SPECS). As per the Union Budget economy survey of 2019-20 the integration of ‘Assemble in India for the World’ into ‘Make in India’, India can raise its export market share to about 3.5% by 2025 and 6% by 2030.

Textile and Apparel:India is among the top garment manufacturing countries in the world. India’s textile exports amounted to US$ 1 billion in September 2022. The government introduced various schemes such as the Scheme for Integrated Textile Parks (SITP), Technology Upgradation Fund Scheme (TUFS), and Mega Integrated Textile Region and Apparel (MITRA) Park scheme. In addition, Amazon India signed an MoU with the Manipur Handloom & Handicrafts Development Corporation Limited (MHHDCL). The sustainable Textiles for Sustainable Development (SusTex) project by the United Nations Climate Change will increase artisans’ engagement from Asia and especially India in the coming decade.

Drugs and Pharmaceuticals: India’s drugs and pharmaceuticals export amounted to US$ 2.1 billion, and it is the largest provider of generic medicines globally. Currently, the country has a share of 20% in the global supply volume and contributes to around 60% of the global vaccines. The USA, the UK, and Russia are among the largest importers from India with a share of 29%, 3%, and 2.4%, respectively during 2021-22. The Strengthening of Pharmaceutical Industry (SPI) scheme focuses on bolstering the existing infrastructure facility, with a total financial outlay of US$ 60 million (Rs. 500 crores).

Marine Products: India’s exports for marine products in September 2022 amounted to US$ 0.7 billion whereinIndia shipped 1,369,264 MT of seafood. Frozen shrimp remained the major export item in terms of quantity and value. The overall export of frozen shrimps during 2021-22 totalled up to 728,123 MT. The USA was the largest market for imported frozen shrimp, followed by China, European Union, South East Asia, Japan, and the Middle East.

Export Promotion Scheme

Foreign Trade Policy 2015-20 and other schemes provide promotional measures to boost India’s exports with the objective to offset infrastructural inefficiencies and associated costs involved to provide exporters a level playing field. Brief of these measures are as under:

1.1 Exports from India Scheme

i. Merchandise Exports from India Scheme (MEIS)

Under this scheme, exports of notified goods/ products to notified markets as listed in Appendix 3B of Handbook of Procedures, are granted freely transferable duty credit scrips on realized FOB value of exports in free foreign exchange at specified rate. Such duty credit scrips can be used for payment of basic custom duties for import of inputs or goods.

Exports of notified goods of FOB value upto Rs 5,00,000 per consignment, through courier or foreign post office using e-commerce shall be entitled for MEIS benefit. List of eligible category under MEIS if exported through using e-commerce platform is available in Appendix 3C.

MEIS has since been withdrawn w.e.f. 1st January, 2021. A new Scheme called Remission of Duties and Taxes on Exported Products (RoDTEP) has been introduced which shall refund the embedded duties suffered in export goods.

ii. Service Exports from India Scheme (SEIS)

Service providers of notified services as per Appendix 3D are eligible for freely transferable duty credit scrip @ 5% of net foreign exchange earned.

2. Duty Exemption & Remission Schemes

These schemes enable duty free import of inputs for export production with export obligation. These scheme consists of:-

2.1 Advance Authorization Scheme

Under this scheme, duty free import of inputs are allowed, that are physically incorporated in the export product (after making normal allowance for wastage) with minimum 15% value addition. Advance Authorization (AA) is issued for inputs in relation to resultant products as per SION or on the basis of self declaration, as per procedures of FTP. AA normally have a validity period of 12 months for the purpose of making imports and a period of 18 months for fulfillment of Export Obligation (EO) from the date of issue. AA is issued either to a manufacturer exporter or merchant exporter tied to a supporting manufacturer(s).

2.2 Advance Authorization for annual requirement

Exporters having past export performance (in at least preceding two financial years) shall be entitled for Advance Authorization for Annual requirement. This shall only be issued for items having SION.

2.3 Duty Free Import Authorization (DFIA) Scheme

DFIA is issued to allow duty free import of inputs, with a minimum value addition requirement of 20%. DFIA shall be exempted only from the payment of basic customs duty. DFIA shall be issued on post export basis for products for which SION has been notified. Separate schemes exist for gems and jewellery sector for which FTP may be referred.

2.4 Duty Drawback of Customs

The scheme is administered by Department of Revenue. Under this scheme products made out of duty paid inputs are first exported and thereafter refund of duty is claimed in two ways:

i) All Industry Rates : As per Schedule

ii) Brand Rate : As per application on the basis of data/documents

2.5 Interest Equalisation Scheme (IES)

The Government announced the Interest Equalisation Scheme @ 3% per annum for Pre and Post Shipment Rupee Export Credit with effect from 1st April, 2015 for 5 years available to all exports under 416 tariff lines [at ITC (HS) code of 4 digit] and exports made by Micro, Small & Medium Enterprises (MSMEs) across all ITC(HS) codes. With effect from November 2, 2018, the rate of Interest Equalisation for MSME has been increased to 5%. The Scheme has also been extended to Merchant Exporters who will now avail the benefit @ 3% for all exports under 416 tariff lines w.e.f. January 2, 2019.

3. EPCG SCHEME

3.1 Zero duty EPCG scheme

Under this scheme import of capital goods at zero custom duty is allowed for producing quality goods and services to enhance India’s export competitiveness. Import under EPCG shall be subject to export obligation equivalent to six times of duty saved in six years. Scheme also allows indigenous sourcing of capital goods with 25% less export obligation.

3.2 Post Export EPCG Duty Credit Scrip Scheme

A Post Export EPCG Duty Credit Scrip Scheme shall be available for exporters who intend to import capital goods on full payment of applicable duty in cash.

4. EOU/EHTP/STP & BTP SCHEMES

Units undertaking to export their entire production of goods and services may be set up under this scheme for import/ procurement domestically without payment of duties. For details of the scheme and benefits available therein FTP may be required.

5. OTHER SCHEMES

5.1 Towns of Export Excellence (TEE)

Selected towns producing goods of Rs. 750 crores or more are notified as TEE on potential for growth in exports and provide financial assistance under MAI Scheme to recognized Associations.

5.2 Market Access Initiative (MAI) Scheme

Under the Scheme, financial assistance is provided for export promotion activities on focus country, focus product basis to EPCs, Industry & Trade Associations, etc. The activities are like market studies/surveys, setting up showroom/warehouse, participation in international trade fairs, publicity campaigns, brand promotion, reimbursement of registration charges for pharmaceuticals, testing charges for engineering products abroad, etc.

5.3 Status Holder Scheme

Upon achieving prescribed export performance, status recognition as one star Export House, two Star Export House, three star export house, four star export house and five star export house is accorded to the eligible applicants as per their export performance. Such Status Holders are eligible for various non-fiscal privileges as prescribed in the Foreign Trade Policy.

In addition to the above schemes, facilities like 24X7 customs clearance, single window in customs, self-assessment of customs duty, prior filing facility of shipping bills etc are available to facilitate exports.

5.4 Gold Card Scheme

The Gold Card Scheme was introduced by the RBI in the year 2004. The Scheme provides for a credit limit for three years, automatic renewal of credit limit, additional 20% limit to meet sudden need of exports on account of additional orders, priority in PCFC, lower charge schedule and fee structure in respect of services provided by Banks, relaxed norms for security and collateral etc,. A Gold Card under the Scheme may be issued to all eligible exporters including those in the small and medium sectors who satisfy the pre-requisite conditions laid by individual Banks.

Apart from the above points, Government has recently unveiled new Trade Policy, link to which has been provided below:

Context: Go first passenger airline has filed for bankruptcy protection recently.

Why Airlines are facing problems?

Ever-increasing number of failing engines supplied by Pratt & Whitney, which it claimed had resulted in half its Airbus fleet being grounded.

Given the high capital and operational costs, the commercial air transport industry operates with wafer thin margins. This has impacted the overall profits of the company.

Since last one-and-half decade, rival airliners have adopted an aggressive pricing strategies to gain market share that stretched balance sheets and made companies more vulnerable to shocks.

External shocks such as COVID crisis and long drawn lockdowns had impacted the operations of many airlines. Similarly, last year’s Ukraine-Russia was has shocked the global prices of oil.

Prolonged rupee’s depreciation against the dollar has sent aviation turbine fuel (ATF) costs soaring for domestic carriers.

Challenges faced by Aviation sector in India

Aviation Industry scenario

Industry trend

Airport Authority of India to spend $ 3 bn on non-metro projects over 2016-2020

$ 3 bn investments in green-field airports – Navi Mumbai and Goa

Authority of India (AAI) has taken up a development programme to spend around INR 25,000 crore in next five years for expansion and modification. Furthermore, Three Public Private Partnership (PPP) airports at Delhi, Hyderabad and Bengaluru have undertaken major expansion plan to the tune of INR 30,000 Crores by 2025. Additionally, INR 36,000 Crores have been planned for investment in the development of new Greenfield airports across the country under PPP mode.

The civil aviation industry in India has emerged as one of the fastest growing industries in the country during the last three years and can be broadly classified into scheduled air transport service which includes domestic and international airlines, non-scheduled air transport service which consists of charter operators and air taxi operators, air cargo service, which includes air transportation of cargo and mail.

In 2010, 79 Mn people travelled to/from/or within India. By 2017 that doubled to 158 mn, and this number is expected to treble to 520 mn by 2037. The nation’s airplane fleet is projected to quadruple in size to approximately 2500 airplanes by 2038.

Currently, the country has 131 operational airports including 29 international, 92 domestic, and 10 custom airports. To meet the growing demand for air travel in India, it has become imperative to increase the capacity of airport infrastructure.

To augment the airport infrastructure the government aims to develop 100 airports by 2024 (under the UDAN Scheme) and expects to invest $1.83 bn in the development of airport infrastructure by 2026.Till date 74 airports have been developed. More than 2.15 lakh UDAN flights have operated and over 1.1 crore passengers have availed the benefits in UDAN flights so far.

The projected upsurge in air travel in India would require more aircraft usage, further igniting the demand for Maintenance, Repair & Overhaul (MRO) services. The Indian Civil Aviation MRO market, at present, stands at around $900 mn and is anticipated to grow to $4.33 bn by 2025 increasing at a CAGR of about 14-15%. Unmanned aerial vehicles, also known as drones have been welcomed across industries. Indian drone industry is expected to have a total turnover of up to US$ 1.8 billion by 2026.

Up to 100% FDI is permitted in Non-scheduled air transport services, Helicopter services and seaplanes under the automatic route.

Up to 100% FDI is permitted in MRO for maintenance and repair organizations; flying training institutes; and technical training institutes under the automatic route.

Government Initiatives

Through the National Civil Aviation Policy 2016 (NCAP) the government plans to take flying to the masses by enhancing affordability and connectivity. It promotes ease of doing business, deregulation, simplified procedures, and e-governance.

In April 2020, the Goods and Services Tax for MRO services rendered locally was reduced from 18% to 5%. The ‘place of supply’ for B2B MRO services was changed to the ‘location of recipient’, enabling Indian MRO facilities to claim zero-rating (i.e., export status) under GST laws on MRO services rendered to prime contractor/OEM located outside India. This has been an extremely crucial policy amendment as it will encourage global participation in the Indian aviation sector by allowing foreign MRO operators to subcontract MRO work to Indian entities without any extra tax liability.

The Regional Connectivity Scheme or UDAN (‘Ude Desh ka Aam Nagrik’) is a vital component of NCAP 2016. The scheme plans to enhance connectivity to India's unserved and under-served airports and envisages to make air travel affordable and widespread. More than 2.15 lakh UDAN flights have operated and over 1.1 Cr passengers have availed the benefits in UDAN flights as on 30th November 2022. The Government has set a target to operationalize 1,000 UDAN routes and to revive/develop 100 unserved & underserved airports/heliports/water aerodromes (including 68 aerodromes) by 2024.

The aircraft leasing and financing businesses are operated from the International Financial Services Centre (IFSC) and GIFT City provides the off-shore status for financial services.

Ministry of Civil Aviation released Krishi UDAN 2.0. The Scheme lays out the vision of improving value realization through better integration and optimization of Agri-harvesting and air transportation and contributing to Agri-value chain sustainability and resilience under different and dynamic conditions. After a 6-month successful pilot of Krishi Udan 2.0 it was decided to add 5 new airports namely Belagavi, Jharsuguda, Jabalpur, Darbhanga and Bhopal to the existing list of 53 airports, taking the number of airports actively participating in Krishi Udan to 58.

Monetising Assets: AAI has formed joint ventures in seven airports. Recently, it awarded six airports — Ahmedabad, Jaipur, Lucknow, Guwahati, Thiruvananthapuram, Mangaluru — for operations, management and development under PPP for a period of 50 years. As per National Monetisation Pipeline (NMP), 25 AAI airports have been earmarked for asset monetisation between 2022 and 2025.

NASP 2022 lays out the vision of making India as one of the top sports nations by 2030, by providing a safe, affordable, accessible, enjoyable, and sustainable air sports ecosystem in India. Air sports, as the names suggests, encompasses various sports activities involving the medium of air. These include sports like air-racing, aerobatics, aero modelling, hang gliding, paragliding, para motoring and skydiving etc.

The Central Government has approved the Production Linked Incentive scheme for drones and drone components. The PLI scheme comes as a follow-through of the liberalized Drone Rules, 2021 released by the Central Government on 25 August 2021. The PLI scheme and new drone rules are intended to catalyze super-normal growth in the upcoming drone sector. The total incentive of INR 120 crores and the total PLI per manufacturer is capped at INR 30 crores.

NABH (NextGen Airports for Bharat): Nirman is a government initiative to expand airport capacity more than five times to handle bn trips a year, in the next 10-15 years.

AAI Startup Policy: Delivering a framework & mechanism for the interaction of AAI with internal and external stakeholders that catalyze innovation at airports and leveraging technology for addressing challenges and enhancing the delivery of services to passengers.

Way forward

Here are some proposals that the government could look at closely to achieve our long-term vision of becoming the biggest aviation market in the world.

1. Tightening the PPP (Public Private Partnership) procurement and concession framework With more private airport concessions on the anvil, there are three things that the government should look at prioritising as part of its reform agenda to enhance competition, attract more foreign investments and deliver better commercial and economic outcomes.

(i) Implement the recommendations of the Kelkar Committee report on revitalizing PPPs (2015), of which two key elements stand out (a) defining triggers and commercial principles for renegotiation of contracts – a necessity in long-tenure concessions with volatile and uncertain market variables (b) disallowing public-sector entities from participating in PPP projects – a good and effective approach to not vitiate the fundamental rationale of private sector procurement

(ii) Providing tariff certainty – an essential tenet in any private sector contract to give comfort to both investors and users.

(iii) Ensure tight procurement timelines – process from tender invitation to award of contracts not exceeding 9 months.

In addition, making airport connectivity or other mobility solutions an integral part of the concession and project agreements. They also need to be co-terminus with airport commencement timelines, with clearly defined obligations and penalty provisions for delays or defaults by contracting parties – the economic costs of non-compliance can be significantly minimized or avoided if properly structured.

2. Redefining our regulatory philosophy With tariff setting and commercial renegotiation mechanisms internalised in PPP contracts, regulators can focus more on monitoring and enforcing the efficient preferred outcomes on service quality, including security, safety and sustainability KPIs that are essential elements of the airport and aviation businesses.

3. Making Air Cargo Infrastructure a national priority Building capacity at Tier-2 and newer airports is now important as well. The UDAN and Krishi UDAN schemes offer great opportunity to build a logistics backbone linking nodal production and distribution centres in the country to serve both domestic and export markets seamlessly and lucratively. The scope for use of unmanned aerial systems (drones) and new mobility solutions (use of urban rail transit for last mile distribution and hyperloop) adds a completely new dimension to the planning, design, implementation and economics of cargo logistics with far reaching implications on utility, safety, security, reliability and viability of services.

4. Rationalizing taxes across the board Below are a few examples of discrepancies and value eroders in our industry that may need a fix:

Withholding taxes (WHT) on aircraft lease rentals –Foreign lessors pass on domestic taxes, including WHT on aircraft lease payments to the Indian carriers, increasing the cost burden. WHT can range from 0-11% of lease rentals subject to availability of double-tax avoidance treaties. Waiver of WHT on lease payments with a sunset clause, would leave more cash in the pockets of carriers and help expedite recovery in a situation where the government is unable to provide direct financial relief.

Rationalising GST on Aviation Turbine Fuel (ATF) – ATF in India costs 30-35% more than neighbouring markets killing airline margins. VAT on ATF varies from 0% to 29% across states in India. This is over and above excise duties, marketing and logistics costs on production and distribution of fuel. Carriers would benefit immensely if ATF is brought under GST with a flat rate of say 5% or lower.

Relief for MRO (Maintenance, Repair, Overhaul) services - Indian carriers spend an estimated USD 1.2 billion every year for MRO services performed abroad because of high tax rates on such services in India. Government recently reduced the GST on aircraft MRO services from 18% to 5% , allowing full input tax credit. But this may not be enough to make Indian carriers change their preferences. Service centres should be stationed in India itself. Other solutions could be: (i) A full waiver of royalty payments for the next five years (NCAP, 2016) (ii) Rationalization of lease rentals charged by airport operators. (iii) A tax incentive for Indian and foreign carriers to procure services in India.

5. Roll-out GAGAN with firm timelines The advantages of GAGAN are many. For example, it would obviate the need to have instrument landing systems (ILS) at smaller airports with limited air-traffic movement, avoid flight diversions, save fuel for airlines and bring down air navigation charges by allowing ground infrastructure and manpower to be optimized. The biggest beneficiaries of this initiative will be general aviation and helicopter operators who depend on visual flight rules (VFR) and are constrained to perform safe and effective night operations.

6. Unlocking value from Open Skies and Liberalized ASAs

Current bilateral air service agreements with some of these countries continue to be restrictive to protect Indian carriers, but it is time for us to take a more pragmatic view of the economic losses associated with this artificial stifling of demand, that is costing us investments, jobs and other multiplier benefits of traffic growth to Tier-2 and Tier-3 cities and towns, especially on routes where domestic carriers may be constrained to deploy reciprocal capacity.

7. Revamping the UDAN scheme The challenge is not demand but the operational and financial sustainability of the program. The solution lies in revamping the scheme to allow newer operators and carriers to come into the system and provide the fleet and flexibility required to deepen regional air travel markets.

1) providing adequate long-term low-cost capital to support new ventures;

2) creating a strong local leasing market;

3) incentivizing use of the NSOP (non-scheduled operators) fleet through code shares; and

4) opening up the industry for air transport aggregators that can significantly multiply the number and frequency of users, much like the ride-hailing market in the urban transport ecosystem, which has transformed intra city travel globally.

8. Making India an aviation manufacturing hub Our challenge has been in moving up and across the manufacturing value chain in the civil aviation industry. For example, the helicopter and small-aircraft market in India is still nascent and can grow exponentially in the next ten years triggered by demands for regional connectivity, medical and emergency services, disaster management and pilot training requirements. The increasing adoption of unmanned aerial systems for commercial and defence purposes presents another unprecedented opportunity for localizing production and globalizing the value chain.

9. Revitalizing India as a global tourist destination

We need to revamp our tourism infrastructure and global marketing initiatives with razor-sharp focus and urgency, especially in a post-COVID world which is likely to trigger a distinct preference for leisure travel and medical tourism. India has plenty to offer on both fronts.

We can triple our foreign tourist arrivals if we get our act together on three strategic elements that have proven to be critical success factors for other tourism economies

(i) High-quality tourism destinations with consistent best in-class infrastructure and state-of-the art mobility solutions (ii) Unrestrained and reliable connectivity options by air and surface transport. (iv) Business friendly fiscal and regulatory environment including friendly visa and immigration policies.

Context: Recently Prominent founders of some of the country’s new-age businesses have accused the Internet and Mobile Association of India (IAMAI) of “promoting the views” of big tech companies such as Google and Meta and have called into question its organisational structure, which is led by representatives of such tech companies.

Why the accusations?

IAMAI criticised the recommendations of the Parliamentary Standing Committee on Finance to introduce a new law for tackling Big Tech firms’ anti-competitive practices.

What were the recommendations of the Parliamentary Penal?

To curb anti-competitive practices in digital markets, last December, the panel proposed measures like having ex-ante regulations, which are meant to protect consumers by requiring companies to follow certain standards of behaviour, as opposed to post-ante regulations that can only punish an entity after it has breached a law.

designating Big Tech entities as “systemically important digital intermediaries” and then subjecting them to certain ex-ante provisions.

a new digital competition law.

It asked digital market entities to desist from “anti-steering”, “deep discounting”, “self-preferencing”, “search & ranking preferencing” and other promotional practices that lead to consumers going for these companies in the market, impacting competition.

Why do we need new digital competition law?

Competition Act, of 2002, covers services but there is ambiguity regarding digital services.

Digital services have a great impact on the consumption of other goods and services this aspect is not covered under the existing Act.

The digital world has a large impact on polity and society as it has become a tool of narrative formation that is being used and misused by political leaders.

We are facing the rising issue of fake news, digital propaganda etc.

Context: Parliamentary committee on Commerce has submitted a report on the status of India’s positive business impression.

Highlights of the report

India has not been able to take advantage of the “China Plus One Strategy,” through which multinationals shifted manufacturing and production away from China.

Southeast Asian countries such as Vietnam, Thailand, Cambodia, and Malaysia have become bigger beneficiaries of the strategy.

India’s competitive position in the pharmaceutical sector is undermined by its high import dependence for bulk drugs or active pharmaceutical ingredients (APIs), especially from China.

In fiscal year 2022-23, till November 30, the value of total import of APIs stood at ₹27,209 crore, out of which imports from China stood at ₹18,973 crore, nearly 70% of the total share.

What is the China Plus 1 strategy: China Plus One or C+1 is the term ascribed to businesses avoiding investing solely in China and diversifying their business into other countries.

Who introduced the China Plus One strategy: The earliest use of the term “China Plus One” can be traced to 2013, but there is no individual to whom the concept has been credited.

What is the Europe Plus One strategy: Similar to the China strategy, Europe Plus One describes European industrialists who are exploring options to relocate their production outside of Europe.

Government’s reply

Government has replied that Production Linked Incentive (PLI) schemes have the capability to make India a more attractive location for companies looking to diversify their supply chains away from China.

It added that more than 3,500 provisions have been decriminalised by the Ministries and the States.

The Jan Vishwas Bill to amend 42 Central Acts has been introduced to enhance trust-based governance.

Committee’s suggestion

Rationalisation of direct taxes and indirect taxes must be done in sync with the international norms and laws to increase the competitiveness of domestic industries in the global markets.

It asked the government to pursue Free or Preferential Trade Agreements with countries that seek to invest in India under the ‘China Plus One Strategy’.